- Bibliography

- More Referencing guides Blog Automated transliteration Relevant bibliographies by topics

- Automated transliteration

- Relevant bibliographies by topics

- Referencing guides

Human resource accounting: a framework for valuation and application.

- Masters Thesis

- Helga Ruth Funk

- Michael Chatfield

- Craig School of Business

- Graduate Business Programs

- California State University, Fresno

- Master of Science in the School of Business and Administrative Sciences

- http://hdl.handle.net/20.500.12680/k930c4937

Items in ScholarWorks are protected by copyright, with all rights reserved, unless otherwise indicated.

Accounting for Human Resources: Implications for Theory and Practice.

PDF Version Also Available for Download.

Description

Knowledge workers are an important resource for the typical modern business firm, yet financial reporting ignores such resources. Some researchers contend that the accounting profession has stressed reliability in order to make the accounting appear objective. Others concur, noting that accounting is an insecure profession and adopts strict rules when faced with uncertainty. Accountants have promulgated a strict rule to expense human resource costs, although many know that such resources have future benefits. Some researchers suggest that any discipline must modify its language in order to initiate change toward providing useful social ameliorations. If accounting theorists extend this idea to … continued below

Creation Information

Stovall, Olin Scott December 2001.

This dissertation is part of the collection entitled: UNT Theses and Dissertations and was provided by the UNT Libraries to the UNT Digital Library , a digital repository hosted by the UNT Libraries . It has been viewed 8175 times, with 8 in the last month. More information about this dissertation can be viewed below.

People and organizations associated with either the creation of this dissertation or its content.

- Stovall, Olin Scott

- Merino, Barbara D. Major Professor

Committee Members

- Luker, William Minor Professor

- Mayper, Alan G., 1952-

- Wu, Frederick H.

- Prybutok, Victor R.

- University of North Texas Place of Publication: Denton, Texas

Rights Holder

For guidance see Citations, Rights, Re-Use .

Provided By

Unt libraries.

The UNT Libraries serve the university and community by providing access to physical and online collections, fostering information literacy, supporting academic research, and much, much more.

Descriptive information to help identify this dissertation. Follow the links below to find similar items on the Digital Library.

Degree Information

- Name: Doctor of Philosophy

- Level: Doctoral

- Discipline: Accounting

- Department: Department of Accounting

- Grantor: University of North Texas

Knowledge workers are an important resource for the typical modern business firm, yet financial reporting ignores such resources. Some researchers contend that the accounting profession has stressed reliability in order to make the accounting appear objective. Others concur, noting that accounting is an insecure profession and adopts strict rules when faced with uncertainty. Accountants have promulgated a strict rule to expense human resource costs, although many know that such resources have future benefits. Some researchers suggest that any discipline must modify its language in order to initiate change toward providing useful social ameliorations. If accounting theorists extend this idea to the accounting lexicon.s description of investments in human resources, investors and other accounting user groups might gain greater insight into how a firm fosters and nourishes human capital. I tested three hypotheses related to this issue by administering an experiment designed to assess financial analysts. perceptions about alternative financial statement treatments of human resources in an investment recommendation task. I predicted that (1) analysts' perceptions of the reliability (relevance) of the information they received would decrease (increase) as the treatment of human resources increasingly violated GAAP (became more current-oriented), (2) analysts exposed to alternative accounting treatments would report a lower likelihood of recommending that their clients invest in the company in the task, and (3) financial analysts who ranked reliability (relevance) as a more important information quality would be less (more) likely to recommend that their clients buy the stock represented in the case because the treatment of human resources on the financial statements violated GAAP (was more current-oriented) as compared to analysts who ranked reliability (relevance) as being lower (higher) in importance. Analysts receiving financial statements with accounting treatments of human resource costs that violated GAAP judged such information as less reliable and were also less likely to recommend that their clients buy the stock in the task than analysts receiving financial statements that conformed to GAAP. Also, analysts who perceived reliability as a more important information quality reacted more negatively to a replacement cost approach to accounting for human resources than participants who perceived reliability as being less important. A potential confounding explanation of the results is the varied language used in the audit opinions included with the treatment financial statements. Whether explained by the audit opinion language or the actual differences contained in the financial statements, the results suggest that an important user group, financial analysts, may be subject to the aura of objectivity suggested by Porter in 1995.

- Human resource accounting

- financial analysts

- objectivity

- relevant experiment

- reliability

Library of Congress Subject Headings

- Human capital -- Accounting.

- Thesis or Dissertation

Unique identifying numbers for this dissertation in the Digital Library or other systems.

- OCLC : 51969862

- Archival Resource Key : ark:/67531/metadc3026

Collections

This dissertation is part of the following collection of related materials.

UNT Theses and Dissertations

Theses and dissertations represent a wealth of scholarly and artistic content created by masters and doctoral students in the degree-seeking process. Some ETDs in this collection are restricted to use by the UNT community .

What responsibilities do I have when using this dissertation?

Digital Files

- 183 image files available in multiple sizes

- 1 file (.pdf)

- Metadata API: descriptive and downloadable metadata available in other formats

Dates and time periods associated with this dissertation.

Creation Date

- December 2001

Added to The UNT Digital Library

- Sept. 25, 2007, 10:58 p.m.

Description Last Updated

- April 14, 2020, 3:19 p.m.

Usage Statistics

When was this dissertation last used?

Interact With This Dissertation

Here are some suggestions for what to do next.

Search Inside

- or search this site for other thesis or dissertations

Start Reading

- All Formats

Citations, Rights, Re-Use

- Citing this Dissertation

- Responsibilities of Use

- Licensing and Permissions

- Linking and Embedding

- Copies and Reproductions

International Image Interoperability Framework

We support the IIIF Presentation API

Print / Share

Links for robots.

Helpful links in machine-readable formats.

Archival Resource Key (ARK)

- ERC Record: /ark:/67531/metadc3026/?

- Persistence Statement: /ark:/67531/metadc3026/??

International Image Interoperability Framework (IIIF)

- IIIF Manifest: /ark:/67531/metadc3026/manifest/

Metadata Formats

- UNTL Format: /ark:/67531/metadc3026/metadata.untl.xml

- DC RDF: /ark:/67531/metadc3026/metadata.dc.rdf

- DC XML: /ark:/67531/metadc3026/metadata.dc.xml

- OAI_DC : /oai/?verb=GetRecord&metadataPrefix=oai_dc&identifier=info:ark/67531/metadc3026

- METS : /ark:/67531/metadc3026/metadata.mets.xml

- OpenSearch Document: /ark:/67531/metadc3026/opensearch.xml

- Thumbnail: /ark:/67531/metadc3026/thumbnail/

- Small Image: /ark:/67531/metadc3026/small/

- In-text: /ark:/67531/metadc3026/urls.txt

- Usage Stats: /stats/stats.json?ark=ark:/67531/metadc3026

Stovall, Olin Scott. Accounting for Human Resources: Implications for Theory and Practice. , dissertation , December 2001; Denton, Texas . ( https://digital.library.unt.edu/ark:/67531/metadc3026/ : accessed August 1, 2024 ), University of North Texas Libraries, UNT Digital Library, https://digital.library.unt.edu ; .

- My Shodhganga

- Receive email updates

- Edit Profile

Shodhganga : a reservoir of Indian theses @ INFLIBNET

- Shodhganga@INFLIBNET

- Dayalbagh Educational Institute

- Department of Accountancy and Law

| Title: | HUMAN RESOURCE ACCOUNTING IN INDIA WITH SPECIFIC REFERENCE TO BHEL AND SAIL |

| Researcher: | Ahuja Reshma |

| Guide(s): | |

| Keywords: | HUMAN RESOURCE ACCOUNTING |

| University: | Dayalbagh Educational Institute |

| Completed Date: | 2007 |

| Abstract: | newline |

| Pagination: | |

| URI: | |

| Appears in Departments: | |

| File | Description | Size | Format | |

|---|---|---|---|---|

| Attached File | 317.45 kB | Adobe PDF | ||

| 240.54 kB | Adobe PDF | |||

| 183.25 kB | Adobe PDF | |||

| 1.42 MB | Adobe PDF | |||

| 613.3 kB | Adobe PDF | |||

| 207.04 kB | Adobe PDF | |||

| 784.87 kB | Adobe PDF | |||

| 732.86 kB | Adobe PDF | |||

| 141.82 kB | Adobe PDF | |||

| 7.61 MB | Adobe PDF | |||

| 7.23 MB | Adobe PDF | |||

| 10.46 MB | Adobe PDF | |||

| 6.89 MB | Adobe PDF | |||

| 1.29 MB | Adobe PDF | |||

| 10.49 MB | Adobe PDF | |||

| 2.92 MB | Adobe PDF | |||

| 2.19 MB | Adobe PDF | |||

| 3 MB | Adobe PDF |

Items in Shodhganga are licensed under Creative Commons Licence Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0).

Academia.edu no longer supports Internet Explorer.

To browse Academia.edu and the wider internet faster and more securely, please take a few seconds to upgrade your browser .

Enter the email address you signed up with and we'll email you a reset link.

- We're Hiring!

- Help Center

Human resource accounting: a historical perspective and future implications

2002, Management Decision

Related Papers

shreelatha H R

Industrial Relations

Gary Sundem

AFRICAN JOURNAL OF BUSINESS MANAGEMENT

Ijaz Bokhari

International Journal of Advanced Research (IJAR)

IJAR Indexing

Human capital creates value by coordinating and managing other capitals to achieve corporate goals. Although intangible, the human factor gives life to entities, creates harmonious environment for improved efficiency, effectiveness and economy in the use of corporate resources. Its usefulness to internal productivity and external goodwill are acknowledged in the literature. Its quality, expertise, experience, character and integrity are attributes sought after by providers of financial and other capitals. Economic benefits flow to the entity from human capital. However, in corporate financial reports, human capital is not an element of the Statement of Financial Position or Balance Statement. Since financial values are not assigned to human resource like other assets, investment in and reward to human capital, which enhance its output, are expensed at the Income Statement level. This practice diminishes its status as the most critical resource of the organization as board chairmen often declare at annual general meetings. Using secondary data, this study supports the findings of previous research works that the assignment of financial values and reflection of human resource in balance sheet, will raise shareholders? wealth and eliminate hidden values in financial reports. Since human capital satisfies the criteria of identifiability and control by an entity set by IAS 38 for Intangible Assets, this study recommends that standard setters and policy makers should commence the process that will lead to the recognition of human capital in balance sheet.

Journal of Human Resource Costing & Accounting

Journal of Environmental, Cultural, Economic and Social Sustainability

Geoff Turner

Even though accounting for an organisation’s human resources was first discussed more than thirty years ago, it is yet to be recognised in mainstream accounting. This paper reviews the history of accounting for human resources and provides support for the continuing development and adoption of the paradigm. Along the way the excuses of an earlier era are refuted and propositions made to legitimise human resource accounting in the next epoch. The accounting profession is challenged to examine its current myopic approach to the provision of decision-making information. It is suggested the profession develop a more inclusive, socially acceptable information system, which includes accounting for human resources, that has its foundation in the measurement of the value created by an organisation for the economic sustainability of itself and its stakeholders.

Alomgir Hossain

Human Resource Accounting (HRA) involves accounting for costs related to human resources as assets as opposed to traditional accounting. Since the beginning of globalization of business and services, human elements are becoming more important input for the success of every organization. The strong growth of international financial reporting standards (IFRS) encourages the consideration of alternative measurement and reporting standards and lends support to the possibility that future financial reports will include non-traditional measurements such as the value of human resources using HRA methods. It helps the management to frame policies for human resources of their organizations. HRA is a process of identifying and measuring data about human resources. It will help to charge human resource investment over a period of time. It is not a new concept in the arena of business world. Economists consider human capital as a production factor, and they explore different ways of measuring its investment. Now accountants are recognizing human resource investment as an asset. This study is build upon Recognition, Measurement and Accounting Treatment of Human Resource Accounting in different organizations.

IOSR Journal of Business and Management

jaynob sarker

francis emeni

It has been increasingly argued in accounting and managerial literature the organization s failure to account for its human resource can have several a' consequences on the overall organizational effectiveness. In this wise the research discussed efforts done in this field by researchers and proposed a model known as I{ identifying and reporting investments made in human resources of an organization are not presently accounted for under conventional accounting practice. This IQR 1 is a three step model which classifies employees into separate Para-homogenous g and determines economic value of the various groups identified and gives the variable determined accounting treatment in the organizations books of account. On applyi1 IQR Model in this study, it was found that, total present value of employees (Junior, Senior) increases from year to year because they acquire skill and knowledge ove1 while on or off-the-job unlike physical assets. Some recommendations were made l on the co...

Jacob Birnberg , James Craft

5 Jacob G. Birnberg and Nicholas Dopuch, A Conceptual Approach to the Framework for Disclosure, Journal of Accountancy, CXV (February, 1963), 59. Also, see Roger H. Hermanson, Accounting for Human Assets, Occasional Paper No. 14, Bureau of Business ...

Loading Preview

Sorry, preview is currently unavailable. You can download the paper by clicking the button above.

RELATED PAPERS

Vijaya Murthy

ijifr journal

Journal of Management Studies

Fariborz Avazzadehfath

Global Journal of Management and Business Research: D Accounting and Auditing

Md. Tanjim Hossain

Dumitru Ionel

Publisher ijmra.us UGC Approved

Legesse Agegnehu

Kavitha C Achar

Olin Stovall

Huaiying Wang

Gürhan Uysal

Journal ijmr.net.in(UGC Approved)

Management Science Letters

Research Journal of Finance and Accounting

Ibukun Falayi

Academy of Management Review

Philip Mirvis

IOSR Journals publish within 3 days

Trang Linh Lê

nader naghshbandi

Simon Kamau

Asian Journal of Finance & Accounting

Australasian Accounting Business and Finance Journal

Vol. 12 No. 8 (2021)

farshad ganji , Hüseyin Arı

RELATED TOPICS

- We're Hiring!

- Help Center

- Find new research papers in:

- Health Sciences

- Earth Sciences

- Cognitive Science

- Mathematics

- Computer Science

- Academia ©2024

Advertisement

Rejuvenating human resource accounting research: a review using bibliometric analysis

- Published: 05 July 2023

Cite this article

- Lakshmi Bhooshetty ORCID: orcid.org/0000-0001-7152-1055 1

467 Accesses

Explore all metrics

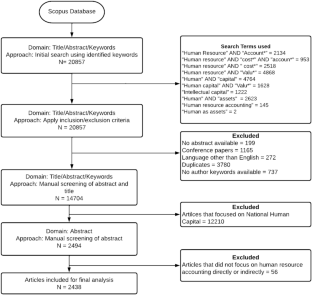

The current study attempts to map the intellectual structure of Human Resource Accounting to understand the research gaps and future trajectories. The study employs systematic literature review technique to extract relevant literature, bibliometric analysis to map the intellectual structure of research in human resource accounting, to identify underlying research themes and content analysis to identify avenues for future research. Based on 2438 publications, author keyword co-occurrences extracted four themes namely, Human Resource Management, Intellectual Capital, Human Capital, and Voluntary Disclosure. The study also summarizes significant findings of papers under each cluster through content analysis identifying areas for future research. The study provides a bird’s eye view of the intellectual structure of academic research efforts in the field of human resource accounting. The study is one of the first attempt to comprehensively review the academic literature from Scopus database employing systematic literature review, bibliometric methods, and content analysis in the field of human resource accounting.

This is a preview of subscription content, log in via an institution to check access.

Access this article

Subscribe and save.

- Get 10 units per month

- Download Article/Chapter or eBook

- 1 Unit = 1 Article or 1 Chapter

- Cancel anytime

Price includes VAT (Russian Federation)

Instant access to the full article PDF.

Rent this article via DeepDyve

Institutional subscriptions

Similar content being viewed by others

Research on environmental accounting: past studies and future trends

Research Trends in Green Human Resource Management: A Comprehensive Review of Bibliometric Data

A bibliometric review of bibliometric reviews of corporate governance: current topics and recommendations for future research

Albrecht SL, Bakker AB, Gruman JA, Macey WH, Saks AM (2015) Employee engagement, human resource management practices and competitive advantage. J Organ Eff People Perform 2(1):7–35. https://doi.org/10.1108/JOEPP-08-2014-0042

Article Google Scholar

Aliyev F, Urkmez T, Wagner R (2019) A comprehensive look at luxury brand marketing research from 2000 to 2016: a bibliometric study and content analysis. Manage Rev Quart 69(3):233–264. https://doi.org/10.1007/s11301-018-00152-3

Alvino F, Di Vaio A, Hassan R, Palladino R (2020) Intellectual capital and sustainable development: a systematic literature review. J Intellect Cap 22(1):76–94. https://doi.org/10.1108/JIC-11-2019-0259

Amalou-Döpke L, Süß S (2014) HR Measurement as an instrument of the HR department in its exchange relationship with top management: a qualitative study based on resource dependence theory. Manage Meas 30(4):444–460. https://doi.org/10.1016/j.scaman.2014.09.003

American Accounting Association Report (1974) Report of the committee on accounting for human resources. Acc Rev 49:115–124

Google Scholar

Ananthram S, Nankervis A, Chan C (2013) Strategic human asset management: evidence from North America. Pers Rev 42(3):281–299. https://doi.org/10.1108/00483481311320417

Archer NP, Ghasemzadeh F, Lynn BE (1998) Performance evaluation in the new economy: Bringing the measurement and evaluation of intellectual capital into the management planning and control system. Int J Technol Manage 16(1–3):162–76. https://doi.org/10.1504/IJTM.1998.002654

Aria M, Cuccurullo C (2017) Bibliometrix: an R-tool for comprehensive science mapping analysis. J Informet 11(4):959–975. https://doi.org/10.1016/j.joi.2017.08.007

Assefa SG, Rorissa A (2013) A bibliometric mapping of the structure of STEM education using co-word analysis. J Am Soc Inform Sci Technol 64(12):2513–2536. https://doi.org/10.1002/asi.22917

Bapna R, Langer N, Mehra A, Gopal R, Gupta A (2013) Human capital investments and employee performance: an analysis of IT services industry. Manage Sci 59(3):641–658. https://doi.org/10.1287/mnsc.1120.1586

Bar-Ilan J (2008) Which H-index?—a comparison of WoS, scopus and google scholar. Scientometrics 74(2):257–271. https://doi.org/10.1007/s11192-008-0216-y

Bartolini M, Bottani E, Grosse EH (2019) Green warehousing: systematic literature review and bibliometric analysis. J Clean Prod 226 (July):242–258. https://doi.org/10.1016/j.jclepro.2019.04.055

Bassett GA (1972) Employee turnover measurement and human resources accounting. Hum Resour Manage (pre-1986_ 11(3):21

Becker B, Gerhart B (1996) The impact of human resource management on organizational performance: progress and prospects. Acad Manag J 39(4):779–801. https://doi.org/10.5465/256712

Bellucci M, Marzi G, Orlando B, Ciampi F (2021) Journal of intellectual capital: a review of emerging themes and future trends. J Intellect Cap 22(4):744–767. https://doi.org/10.1108/JIC-10-2019-0239

Bessieux-Ollier C, Nègre E, Verdier M-A (2022) Moving from accounting for people to accounting with people: a critical analysis of the literature and avenues for research. Eur Acc Rev. https://doi.org/10.1080/09638180.2022.2052922

Bharathi Kamath G (2008) Intellectual capital and corporate performance in Indian pharmaceutical industry. J Intellect Cap 9(4):684–704. https://doi.org/10.1108/14691930810913221

Block J, Fisch C, Rehan F (2020) Religion and entrepreneurship: a map of the field and a bibliometric analysis. Manage Rev Quart 70(4):591–627. https://doi.org/10.1007/s11301-019-00177-2

Bontis N (1999) Managing organizational knowledge by diagnosing intellectual capital: framing and advancing the state of the field. Int J Technol Manag 18:433–462

Bontis N, Fitz-enz J (2002) Intellectual capital ROI: a causal map of human capital antecedents and consequents. J Intellect Cap 3(3):223–247. https://doi.org/10.1108/14691930210435589

Bontis N, Serenko A (2009) A causal model of human capital antecedents and consequents in the financial services industry. Edited by Nick Bontis and Christopher Bart. J Intell Cap 10(1):53–69. https://doi.org/10.1108/14691930910922897

Bontis N, Janošević S, Dženopoljac V (2015) Intellectual capital in Serbia’s hotel industry. Int J Contemp Hosp Manag 27(6):1365–1384. https://doi.org/10.1108/IJCHM-12-2013-0541

Boxall P, Macky K (2007) High-performance work systems and organisational performance: bridging theory and practice. Asia Pac J Hum Resour 45(3):261–270. https://doi.org/10.1177/1038411107082273

Bradford SC (1934) Sources of information on specific subjects. Engineering 137:85–86

Brummet RL, Flamholtz EG, Pyle WC (1968) Human resource measurement – a challenge for accountants. Acc Rev 43(2):217–224

Bullay A, Abuhommous AA, Kukreja G (2021) The relationship between intellectual capital and employees’ productivity: evidence from the gulf cooperation council. J Manage Dev 40(6):526–541. https://doi.org/10.1108/JMD-05-2019-0210

Caddy I (2002) Issues concerning intellectual capital metrics and measurement of intellectual capital. Singap Manag Rev 24(3):77–88

Camuffo A, Comacchio A (2005) Linking intellectual capital and competitive advantage: a cross-firm competence model for North-East Italian SMEs in the manufacturing industry. Hum Resour Dev Int 8(3):361–377. https://doi.org/10.1080/13678860500149951

Cannon JA (1974) A further comment on human resource accounting. Pers Rev 3(4):38–42. https://doi.org/10.1108/eb055267

Caves RE (1980) Industrial organization, corporate strategy and structure. In: Emmanuel C, Otley D, Merchant K (eds) Readings in accounting for management control. Springer, Boston, pp 335–370. https://doi.org/10.1007/978-1-4899-7138-8_16

Chapter Google Scholar

Chandler GN, Hanks SH (1998) An examination of the substitutability of founders human and financial capital in emerging business ventures. J Bus Vent 13(5):353–369. https://doi.org/10.1016/S0883-9026(97)00034-7

Chen X, Wang S, Tang Y, Hao T (2018) A bibliometric analysis of event detection in social media. Online Inf Rev 43(1):29–52. https://doi.org/10.1108/OIR-03-2018-0068

Cheng B, Wang M, Mørch AI, Chen N-S, Spector JM (2014) Research on E-learning in the workplace 2000–2012: a bibliometric analysis of the literature. Educ Res Rev 11:56–72. https://doi.org/10.1016/j.edurev.2014.01.001

Chung Y, Colakoglu S (2018) A closer examination of how human resource management systems impact social and human capital in organisations. Int J Learn Intellect Cap 15(2):119–136. https://doi.org/10.1504/IJLIC.2018.091977

Coff RW (1999) How buyers cope with uncertainty when acquiring firms in knowledge-intensive industries: caveat emptor. Organ Sci 10(2):144–161

Collis DJ, Montgomery CA (1995) How do you create and sustain a profitable strategic? Competing on resources. Harv Bus Rev 73(4):118–128

Comerio N, Strozzi F (2019) Tourism and Its economic impact: a literature review using bibliometric tools. Tour Econ 25(1):109–131. https://doi.org/10.1177/1354816618793762

Couckuyt D, Van Looy A (2019) Green BPM as a business-oriented discipline: a systematic mapping study and research agenda. Sustainability 11(15):4200. https://doi.org/10.3390/su11154200

Criaco G, Minola T, Migliorini P, Serarols-Tarrés C (2014) ‘To have and have not’: founders’ human capital and university start-up survival. J Technol Transf 39(4):567–593. https://doi.org/10.1007/s10961-013-9312-0

Dammak S (2015) Human capital disclosure and market capitalization. Corp Ownersh Control 13(1):502–513. https://doi.org/10.22495/cocv13i1c4p8

Daum JH (2003) Intangible assets and value creation. John Wiley & Sons

Davenport TH, Harris J, Shapiro J (2010) Competing on talent analytics. Harv Bus Rev 88(10):52–58

De Saá-Pérez P, GarcÍa-FalcÓn JM (2002) A resource-based view of human resource management and organizational capabilities development. Int J Hum Resour Manage 13(1):123–140. https://doi.org/10.1080/09585190110092848

De Winne S, Sels L (2010) Interrelationships between human capital, HRM and innovation in belgian start-ups aiming at an innovation strategy. Int J Hum Resour Manage 21(11):1863–1883. https://doi.org/10.1080/09585192.2010.505088

Delery JE, Roumpi D (2017) Strategic human resource management, human capital and competitive advantage: is the field going in circles? Hum Resour Manag J 27(1):1–21. https://doi.org/10.1111/1748-8583.12137

Ding Y, Chowdhury GG, Foo S (2001) Bibliometric cartography of information retrieval research by using co-word analysis. Inf Process Manage 37(6):817–842. https://doi.org/10.1016/S0306-4573(00)00051-0

dos Santos NMBF, Nunes D, Freitas FCR, Munhoz IP, Caldana A (2019) Human capital measurement: a bibliometric survey. In: Iano Y, Arthur R, Saotome O, Estrela VV, Loschi HJ (eds) Proceedings of the 4th Brazilian technology symposium (BTSym’18), pp 451–459. Smart Innovation, Systems and Technologies. Springer International Publishing, Cham https://doi.org/10.1007/978-3-030-16053-1_43

Dzenopoljac V, Yaacoub C, Elkanj N, Bontis N (2017) Impact of intellectual capital on corporate performance: evidence from the Arab region. J Intellect Cap 18(4):884–903. https://doi.org/10.1108/JIC-01-2017-0014

Dzinkowski R (2000) The measurement and management of intellectual capital: an introduction. Manage Acc 78(2):32–36

Edvinsson L (1997) Developing intellectual capital at Skandia. Long Range Plan 30:10

Elbannan MA, Farooq O (2016) Value relevance of voluntary human capital disclosure: european evidence. J Appl Bus Res (JABR) 32(6):1555–1560. https://doi.org/10.19030/jabr.v32i6.9807

Estrin S, Mickiewicz T, Stephan U (2016) Human capital in social and commercial entrepreneurship. J Bus Ventur 31(4):449–467. https://doi.org/10.1016/j.jbusvent.2016.05.003

Fahimnia B, Sarkis J, Davarzani H (2015) Green supply chain management: a review and bibliometric analysis. Int J Prod Econ 162(April):101–114. https://doi.org/10.1016/j.ijpe.2015.01.003

Ferguson DH, Berger F (1985) Employees as assets: a fresh approach to human-resources accounting. Cornell Hotel Restaur Adm Quart 25(4):24–29. https://doi.org/10.1177/001088048502500407

Fernandez V, Maureen L, Nicolas C, Merigó JM, Arroyo-Cañada F-J (2019) Industrial marketing research: a bibliometric analysis (1990–2015). J Bus Ind Mark 34(3):550–560. https://doi.org/10.1108/JBIM-07-2017-0167

Filios VP (1991) Human resource accounting is social accounting: a managerial reappraisal. Hum Syst Manag 10(4):267–280. https://doi.org/10.3233/HSM-1991-10405

Fisch C, Block J (2018) Six tips for your (systematic) literature review in business and management research. Manage Rev Quart 68(2):103–106. https://doi.org/10.1007/s11301-018-0142-x

Fitz-enz J (2010) The new HR analytics: predicting the economic value of your company’s human capital investments. American Management Association, New York

Flamholtz E (1972) Human resource accounting: a review of theory and research. Acad Manag Proc 1:174–177. https://doi.org/10.5465/ambpp.1972.4981436

Flamholtz E (1976) The impact of human resource valuation on management decisions: a laboratory experiment. Acc Organ Soc 1(2–3):153–165. https://doi.org/10.1016/0361-3682(76)90019-2

Flamholtz EG (1980) The process of measurement in managerial accounting: a psycho-technical systems perspective. Acc Organ Soc 5(1):31–42. https://doi.org/10.1016/0361-3682(80)90019-7

Flamholtz EG, Main ED (1999) Current issues, recent advancements, and future directions in human resource accounting. J Hum Resour Cost Acc 4(1):11–20. https://doi.org/10.1108/eb029050

Flamholtz EG, Bullen ML, Hua W (2002) Human resource accounting: a historical perspective and future implications. Manag Decis 40(10):947–954. https://doi.org/10.1108/00251740210452818

Flamholtz EG, Kannan-Narasimhan R, Bullen ML (2004) Human resource accounting today: contributions, controversies and conclusions. J Hum Resour Cost Acc 8(2):23–37. https://doi.org/10.1108/eb029084

Fulmer IS, Ployhart RE (2014) ‘Our most important asset’: a multidisciplinary/multilevel review of human capital valuation for research and practice. J Manag 40(1):161–192. https://doi.org/10.1177/0149206313511271

Galunic DC, Anderson E (2000) From security to mobility: generalized investments in human capital and agent commitment. Organ Sci 11(1):1–20. https://doi.org/10.1287/orsc.11.1.1.12565

Gamerschlag R, Moeller K (2011) The positive effects of human capital reporting. Corp Reput Rev 14(2):145–155. https://doi.org/10.1057/crr.2011.11

Gross-Gołacka E, Kusterka-Jefmańska M, Jefmański B (2020) Can elements of intellectual capital improve business sustainability?—The perspective of managers of SMEs in Poland. Sustainability 12(4):1545. https://doi.org/10.3390/su12041545

Gupta BM, Dhawan SM (2009) Status of India in science and technology as reflected in its publication output in the scopus international database, 1996–2006. Scientometrics 80(2):473–490. https://doi.org/10.1007/s11192-008-2083-y

Guthrie J, Petty R (2000) Intellectual capital: australian annual reporting practices. J Intellect Cap 1(3):241–251

Hayton JC (2005) Competing in the new economy: the effect of intellectual capital on corporate entrepreneurship in high-technology new ventures. R&D Manage 35(2):137–155. https://doi.org/10.1111/j.1467-9310.2005.00379.x

Hekimian JS, Jones CH (1967) Put people on your balance sheet. Harvard Bus Rev 45:105–113

Hirsch JE (2005) An index to quantify an individual’s scientific research output. Proc Natl Acad Sci 102(46):16569–16572. https://doi.org/10.1073/pnas.0507655102

Hormiga E, Batista-Canino RM, Sánchez-Medina A (2011) The role of intellectual capital in the success of new ventures. Int Entrep Manage J 7(1):71–92. https://doi.org/10.1007/s11365-010-0139-y

Huang C-F, Hsueh S-L (2007) A study on the relationship between intellectual capital and business performance in the engineering consulting industry: a path analysis. J Civ Eng Manag 13(4):265–271. https://doi.org/10.3846/13923730.2007.9636446

Jain J, Walia N, Singh S, Jain E (2021) Mapping the field of behavioural biases: a literature review using bibliometric analysis. Manage Rev Quart. https://doi.org/10.1007/s11301-021-00215-y

Jia H, Zhou S, Allaway AW (2018) Understanding the evolution of consumer psychology research: a bibliometric and network analysis. J Consum Behav 17(5):491–502. https://doi.org/10.1002/cb.1734

Johnson WHA (2002) Leveraging intellectual capital through product and process management of human capital. J Intellect Cap 3(4):415–429. https://doi.org/10.1108/14691930210448323

Jones DMC (1973) Accounting for human assets. Manag Decis 11(3):183–194. https://doi.org/10.1108/eb001021

Joshi M, Cahill D, Sidhu J, Kansal M (2013) Intellectual capital and financial performance: an evaluation of the australian financial sector. J Intellect Cap 14(2):264–285. https://doi.org/10.1108/14691931311323887

Juma N, McGEE J (2006) The relationship between intellectual capital and new venture performance: an empirical investigation of the moderating role of the environment. Int J Innov Technol Manag 03(04):379–405. https://doi.org/10.1142/S0219877006000892

Kamath GB (2021) Corporate governance and intellectual capital disclosure. Int J Learn Intellect Cap 18(4):365–398. https://doi.org/10.1504/IJLIC.2021.118412

Kaplan RS, Norton DP (2006) Alignment: using the balanced scorecard to create corporate synergies – Kaplan RS, Norton DP (eds). Harvard Business School Press, Boston

Kent Baker H, Pandey N, Kumar S, Haldar A (2020) A bibliometric analysis of board diversity: current status, development, and future research directions. J Bus Res 108(January):232–246. https://doi.org/10.1016/j.jbusres.2019.11.025

Komnenic B, Pokrajčić D (2012) Intellectual capital and corporate performance of MNCs in Serbia. J Intellect Cap 13(1):106–119. https://doi.org/10.1108/14691931211196231

Kouhy R, Vedd R (2000) Performance measurement in strategic human resource management. Int J Bus Perform Manage 2(1/2/3):137. https://doi.org/10.1504/IJBPM.2000.000073

Kryscynski D, Coff R, Campbell B (2021) Charting a path between firm-specific incentives and human capital-based competitive advantage. Strateg Manag J 42(2):386–412. https://doi.org/10.1002/smj.3226

Kumar S, Sureka R, Colombage S (2020) Capital structure of SMEs: a systematic literature review and bibliometric analysis. Manage Rev Quart 70(4):535–565. https://doi.org/10.1007/s11301-019-00175-4

Lajili K, Zéghal D (2006) Market performance impacts of human capital disclosures. J Acc Public Policy 25(2):171–194. https://doi.org/10.1016/j.jaccpubpol.2006.01.006

Lardo A, Dumay J, Trequattrini R, Russo G (2017) Social media networks as drivers for intellectual capital disclosure. J Intellect Cap 18(1):63–80. https://doi.org/10.1108/JIC-09-2016-0093

Leifheit N, Follert F (2021) Financial player valuation from the perspective of the club: the case of football. Manag Sport Leisure. https://doi.org/10.1080/23750472.2021.1944821

Leitner K-H (2011) The effect of intellectual capital on product innovativeness in SMEs. Int J Technol Manage 53(1):1–18. https://doi.org/10.1504/IJTM.2011.037235

Lev B (2001) Intangibles: management, measurement, and reporting. Brookings Institution Press

Lev B, Schwartz A (1971) On the use of the economic concept of human capital in financial statements. Account Rev 46(1):103–112

Li C, Kening Wu, Jingyao Wu (2017) A Bibliometric Analysis of Research on Haze during 2000–2016. Environ Sci Pollut Res 24(32):24733–24742. https://doi.org/10.1007/s11356-017-0440-1

Likert R, Pyle WC (1971) A human organizational measurement approach. Financ Anal J 27(1):75–84

Lin CYY, Wei YC, Chen MH (2006) The role of board chair in the relationship between board human capital and firm performance. Int J Bus Gov Ethics 2(3/4):329. https://doi.org/10.1504/IJBGE.2006.011161

Macpherson A, Holt R (2007) Knowledge, learning and small firm growth: a systematic review of the evidence. Res Policy 36(2):172–192. https://doi.org/10.1016/j.respol.2006.10.001

Maditinos D, Chatzoudes D, Tsairidis C, Theriou G (2011) The impact of intellectual capital on firms’ market value and financial performance. J Intellect Cap 12(1):132–151. https://doi.org/10.1108/14691931111097944

Mao G, Huang N, Chen L, Wang H (2018) Research on biomass energy and environment from the past to the future: a bibliometric analysis. Sci Total Environ 635:1081–1090. https://doi.org/10.1016/j.scitotenv.2018.04.173

Mardini GH, Lahyani FE (2022) Impact of firm performance and corporate governance mechanisms on intellectual capital disclosures in CEO statements. J Intellect Cap 23(2):290–312. https://doi.org/10.1108/JIC-02-2020-0053

Martin BC, McNally JJ, Kay MJ (2013) Examining the formation of human capital in entrepreneurship: a meta-analysis of entrepreneurship education outcomes. J Bus Ventur 28(2):211–224. https://doi.org/10.1016/j.jbusvent.2012.03.002

Martín-de-Castro G, Delgado-Verde M, López-Sáez P, Navas-López JE (2011) Towards ‘an intellectual capital-based view of the firm’: origins and nature. J Bus Ethics 98(4):649–662. https://doi.org/10.1007/s10551-010-0644-5

Mavridis DG, Kyrmizoglou P (2005) Intellectual capital performance drivers in the greek banking sector. Manag Res News 28(5):43–62. https://doi.org/10.1108/01409170510629032

McGuirk H, Lenihan H, Hart M (2015) Measuring the impact of innovative human capital on small firms’ propensity to innovate. Res Policy 44(4):965–976. https://doi.org/10.1016/j.respol.2014.11.008

Mehralian G, Rajabzadeh A, Sadeh MR, Rasekh HR (2012) Intellectual capital and corporate performance in iranian pharmaceutical industry. J Intellect Cap 13(1):138–158. https://doi.org/10.1108/14691931211196259

Michael Hall C (2011) Publish and perish? Bibliometric analysis, journal ranking and the assessment of research quality in Tourism. Tour Manage 32(1):16–27. https://doi.org/10.1016/j.tourman.2010.07.001

Mihardjo LWW, Jermsittiparsert K, Ahmed U, Chankoson T, Hussain HI (2021) Impact of key HR practices (human capital, training and rewards) on service recovery performance with mediating role of employee commitment of the takaful industry of the Southeast Asian Region. Educ Train 63(1):1–21. https://doi.org/10.1108/ET-08-2019-0188

Mishra D, Gunasekaran A, Papadopoulos T, Childe SJ (2016) Big data and supply chain management: a review and bibliometric analysis. Ann Oper Res 270(1–2):313–336. https://doi.org/10.1007/s10479-016-2236-y

Mondal A, Ghosh SK (2012) Intellectual capital and financial performance of Indian Banks. J Intellect Cap 13(4):515–530. https://doi.org/10.1108/14691931211276115

Mouritsen J (2004) Measuring and intervening: how do we theorise intellectual capital management? J Intellect Cap 5(2):257–267. https://doi.org/10.1108/14691930410533687

Nguyen AH, Doan DT (2020) The impact of intellectual capital on firm value: empirical evidence from Vietnam. Int J Financ Res 11(4):74. https://doi.org/10.5430/ijfr.v11n4p74

Ni Y, Cheng Y-R, Huang P (2021) Do intellectual capitals matter to firm value enhancement? Evidences from Taiwan. J Intellect Cap 22(4):725–743. https://doi.org/10.1108/JIC-10-2019-0235

Nieves J, Quintana A, Osorio J (2014) Knowledge-based resources and innovation in the hotel industry. Int J Hosp Manag 38(April):65–73. https://doi.org/10.1016/j.ijhm.2014.01.001

Nimtrakoon S (2015) The relationship between intellectual capital, firms’ market value and financial performance. J Intellect Cap 16(3):587–618. https://doi.org/10.1108/JIC-09-2014-0104

O’Donnell L, Kramar R, Dyball MC (2009) Human capital reporting: should it be industry specific? Asia Pac J Hum Resour 47(3):358–373. https://doi.org/10.1177/1038411108099293

Offstein EH, Gnyawali DR, Cobb AT (2005) A strategic human resource perspective of firm competitive behavior. Hum Resour Manag Rev 15(4):305–318. https://doi.org/10.1016/j.hrmr.2005.11.007

Oprean V-B, Oprisor T (2014) Accounting for soccer players: capitalization paradigm versus expenditure. Proc Econ Finance 15:1647–1654. https://doi.org/10.1016/S2212-5671(14)00636-4

Ozkan N, Cakan S, Kayacan M (2017) Intellectual capital and financial performance: a study of the Turkish banking sector. Borsa Istanbul Rev 17(3):190–198. https://doi.org/10.1016/j.bir.2016.03.001

Peña I (2002) Intellectual capital and business start-up success. J Intellect Cap 3(2):180–198. https://doi.org/10.1108/14691930210424761

Persson O (2009) Celebrating scholarly communication studies. Int Soc Scientometr Informetr 5:9–24

Phusavat K, Comepa N, Sitko-Lutek A, Ooi K-B (2011) Interrelationships between intellectual capital and performance. Ind Manag Data Syst 111(6):810–829. https://doi.org/10.1108/02635571111144928

Pisano S, Lepore L, Lamboglia R (2017) Corporate disclosure of human capital via linkedin and ownership structure. J Intellect Cap 18(1):102–127. https://doi.org/10.1108/JIC-01-2016-0016

Qamar Y, Samad TA (2022) Human resource analytics: a review and bibliometric analysis. Pers Rev 51(1):251–283. https://doi.org/10.1108/PR-04-2020-0247

Quintero-Quintero W, Blanco-Ariza AB, Garzón-Castrillón MA (2021) Intellectual capital: a review and bibliometric analysis. Publications. https://doi.org/10.3390/publications9040046

Radhakrishna RB, Jackson GB (1995) Prolific authors in the journal of agricultural education: a review of the eighties. J Agric Educ 36(1):9

Ramli A, Rasdi RM (2021) Leveraging Intellectual Capital Dimensions for Promoting Learning Organization in a Rural Development Agency. Pertanika J Soc Sci Humanit. https://doi.org/10.47836/pjssh.29.1.37

Ramos-Rodríguez A-R, Ruíz-Navarro J (2004) Changes in the intellectual structure of strategic management research: a bibliometric study of the strategic management journal, 1980–2000. Strateg Manag J 25(10):981–1004. https://doi.org/10.1002/smj.397

Rana S, Pragati (2022) A bibliometric and visualization analysis of human capital and sustainability. Vision. https://doi.org/10.1177/09722629221105773

Rodrigues H, Almeida F, Figueiredo V, Lopes SL (2019) Tracking E-learning through published papers: a systematic review. Comput Educ 136(July):87–98. https://doi.org/10.1016/j.compedu.2019.03.007

Sadabadi AA, Ramezani S, Fartash K, Nikijoo I (2022) Intangible assets: scientometrics and bibliometric using social network analysis. Int J Inf Sci Manage (IJISM) 20(4):49–73

Samson K, Bhanugopan R (2022) Strategic human capital analytics and organisation performance: the mediating effects of managerial decision-making. J Bus Res 144(May):637–649. https://doi.org/10.1016/j.jbusres.2022.01.044

Secinaro S, Brescia V, Calandra D, Biancone P (2020) Employing bibliometric analysis to identify suitable business models for electric cars. J Clean Prod 264:121503. https://doi.org/10.1016/j.jclepro.2020.121503

Secundo G, Margherita A, Elia G, Passiante G (2010) Intangible assets in higher education and research: mission, performance or both?. Edited by Eric Kong. J Intellect Cap 11(2):140–157. https://doi.org/10.1108/14691931011039651

Seetharaman A, Sooria HHBZ, Saravanan AS (2002) Intellectual capital accounting and reporting in the knowledge economy. J Intellect Cap 3(2):128–148. https://doi.org/10.1108/14691930210424734

Sihotang P, Winata A (2008) The intellectual capital disclosures of technology-driven companies: evidence from indonesia. Int J Learn Intellect Cap 5(1):63–82. https://doi.org/10.1504/IJLIC.2008.018883

Singla HK (2020) Does VAIC affect the profitability and value of real estate and infrastructure firms in India? A panel data investigation. J Intellect Cap 21(3):309–331. https://doi.org/10.1108/JIC-03-2019-0053

Smith ME (2003) Another road to evaluating knowledge assets. Hum Resour Dev Rev 2(1):6–25. https://doi.org/10.1177/1534484302250598

Soewarno N, Tjahjadi B (2020) Measures that matter: an empirical investigation of intellectual capital and financial performance of banking firms in Indonesia. J Intellect Cap 21(6):1085–1106. https://doi.org/10.1108/JIC-09-2019-0225

Sollosy M, McInerney M, Braun CK (2016) Human capital: a strategic asset whose time has come to be recognized on organizations’ financial statements. J Corp Acc Finance 27(6):19–27. https://doi.org/10.1002/jcaf.22201

Sonnier BM (2008) Intellectual capital disclosure: high-tech versus traditional sector companies. J Intellect Cap 9(4):705–722. https://doi.org/10.1108/14691930810913230

Stewart T (1991) BRAINPOWER intellectual capital is becoming corporate America’s most valuable asset and can be its sharpest competitive weapon. The Challenge Is to Find What You Have -- and Use It. - June 3, 1991.” 1991. https://archive.fortune.com/magazines/fortune/fortune_archive/1991/06/03/75096/index.htm

Stewart T (1994) Your company’s most valuable asset: intellectual capital business pioneers are finding surprising ways to put real dollars on the bottom line as they discover how to measure and manage the ultimate intangible: knowledge. - October 3, 1994.” 1994. https://money.cnn.com/magazines/fortune/fortune_archive/1994/10/03/79803/

Stewart TA (1997) Intellectual capital: the new wealth of organizations, 1st edn. Doubleday/Currency, New York

Stovel M, Bontis N (2002) Voluntary turnover: knowledge management – friend or foe? J Intellect Cap. https://doi.org/10.1108/14691930210435633

Sydler R, Haefliger S, Pruksa R (2014) Measuring intellectual capital with financial figures: can we predict firm profitability? Eur Manag J 32(2):244–259. https://doi.org/10.1016/j.emj.2013.01.008

Teece DJ, Pisano G, Shuen A (1997) Dynamic capabilities and strategic management. Strat Manage J 18(7):509–533

Tobin J (1969) A general equilibrium approach to monetary theory. J Money Credit Bank 1(1):15–29. https://doi.org/10.2307/1991374

Tunc Bozbura F (2004) Measurement and application of intellectual capital in Turkey. Learn Organ 11(4/5):357–367. https://doi.org/10.1108/09696470410538251

Van Eck NJ, Waltman L (2014) Visualizing bibliometric networks. In: Ding Y, Rousseau R, Wolfram D (eds) Measuring scholarly impact. Springer International Publishing, Cham, pp 285–320. https://doi.org/10.1007/978-3-319-10377-8_13

Vergauwen P, Bollen L, Oirbans E (2007) Intellectual capital disclosure and intangible value drivers: an empirical study. Manag Decis 45(7):1163–1180. https://doi.org/10.1108/00251740710773961

Vishnu S, Gupta VK (2014) Intellectual capital and performance of pharmaceutical firms in India. J Intellect Cap 15(1):83–99. https://doi.org/10.1108/JIC-04-2013-0049

Walsh K, Enz CA, Canina L (2008) The impact of strategic orientation on intellectual capital investments in customer service firms. J Serv Res 10(4):300–317. https://doi.org/10.1177/1094670508314285

Wang X, Hou Y, Cullinane N (2015) How does the human resource department’s client relationship management impact on organizational performance in China? Mediate effect of human capital. S Afr J Econ Manage Sci 18(3):291–307. https://doi.org/10.17159/2222-3436/2015/V18N3A1

Welpe I, Rachbauer S (2006) What is different in human capital management? The necessity and advantages of a new philosophy for human resource departments. Int J Learn Intellect Cap 3(4):421. https://doi.org/10.1504/IJLIC.2006.011750

Wernerfelt B (1984) A resource-based view of the firm. Strateg Manag J 5(2):171–180. https://doi.org/10.1002/smj.4250050207

Wiig KM (1997) Integrating intellectual capital and knowledge management. Long Range Plan 30:7

Winter SG, Nelson RR (1982) An Evolutionary Theory of Economic Change. SSRN Scholarly Paper ID 1496211. Rochester, NY: Social Science Research Network. https://papers.ssrn.com/abstract=1496211

Wright PM, McMahan GC, McWilliams A (1994) Human resources and sustained competitive advantage: a resource-based perspective. Int J Hum Resour Manage 5(2):301–326. https://doi.org/10.1080/09585199400000020

Xu XL, Chen HH, Zhang RR (2020) The impact of intellectual capital efficiency on corporate sustainable growth-evidence from smart agriculture in China. Agriculture 10(6):199. https://doi.org/10.3390/agriculture10060199

Yang C-C, Lin C-Y (2009) Does intellectual capital mediate the relationship between HRM and organizational performance? Perspective of a healthcare industry in Taiwan. Int J Hum Resour Manage 20(9):1965–1984. https://doi.org/10.1080/09585190903142415

Yong JY, Yusliza M-Y, Ramayah T, Fawehinmi O (2019) Nexus between green intellectual capital and green human resource management. J Clean Prod 215(April):364–374. https://doi.org/10.1016/j.jclepro.2018.12.306

Zehir C, Gurol Y, Karaboga T, Kole M (2016) Strategic human resource management and firm performance: the mediating role of entrepreneurial orientation. Proc Soc Behav Sci 235(November):372–381. https://doi.org/10.1016/j.sbspro.2016.11.045

Zhao Y, Ruan W, Jiang Y, Rao J (2018) Salesperson human capital investment and heterogeneous export enterprises performance. J Bus Econ Manag 19(4):609–629. https://doi.org/10.3846/jbem.2018.6267

Zucker LG, Darby MR (1996) Star Scientists and Institutional Transformation: Patterns of Invention and Innovation in the Formation of the Biotechnology Industry. Proc Natl Acad Sci USA 93(23):12709–12716

Download references

The authors declare that no funds, grants, or other support were received during the preparation of this manuscript.

Author information

Authors and affiliations.

Department of Commerce, Christ University, Bangalore, India

Lakshmi Bhooshetty

You can also search for this author in PubMed Google Scholar

Contributions

The paper was authored by a single author.

Corresponding author

Correspondence to Lakshmi Bhooshetty .

Ethics declarations

Conflict of interest.

The author has no relevant financial or non-financial interests to disclose.

Data availability statements

The data that support the findings of this study are available from the corresponding author upon request.

Additional information

Publisher's note.

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

Reprints and permissions

About this article

Bhooshetty, L. Rejuvenating human resource accounting research: a review using bibliometric analysis. Manag Rev Q (2023). https://doi.org/10.1007/s11301-023-00357-1

Download citation

Received : 23 October 2021

Accepted : 12 June 2023

Published : 05 July 2023

DOI : https://doi.org/10.1007/s11301-023-00357-1

Share this article

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

- Human resource accounting

- Bibliometric analysis

- Author keyword co-occurrences

- Network visualization

JEL Classification

- Find a journal

- Publish with us

- Track your research

HUMAN RESOURCE ACCOUNTING AND FINANCIAL PERFORMANCE OF SELECTED QUOTED NIGERIAN FOOD AND BEVERAGES FIRMS

- October 2022

- Finance & Accounting Research Journal 4(3):51-57

- CC BY-NC 4.0

- This person is not on ResearchGate, or hasn't claimed this research yet.

- Delta State University, Abraka

Abstract and Figures

Discover the world's research

- 25+ million members

- 160+ million publication pages

- 2.3+ billion citations

- Tolulope Olaitan Sule

- I R Akintoye

- I J Manukaji

- B C Osisioma

- P V C Okoye

- P C Eze-Nwosu

- Recruit researchers

- Join for free

- Login Email Tip: Most researchers use their institutional email address as their ResearchGate login Password Forgot password? Keep me logged in Log in or Continue with Google Welcome back! Please log in. Email · Hint Tip: Most researchers use their institutional email address as their ResearchGate login Password Forgot password? Keep me logged in Log in or Continue with Google No account? Sign up

Home > Colleges & Schools > Soules College of Business > Human Resource Development > HRD_GRAD

Human Resource Development Theses and Dissertations

Theses/dissertations from 2023 2023.

CAMPUS-LEVEL TEACHER TURNOVER IN TEXAS PUBLIC ELEMENTARY SCHOOLS: AN EXAMINATION OF THE IMPACT OF LEADERSHIP FACTORS AND SCHOOL DEMOGRAPHICS USING HEIRARCHICAL LINEAR MODELING , Amy Welch Baskin

HUMAN RESOURCE DEVELOPMENT PROFESSIONALS’ COMPETENCIES AND CAREER SUCCESS IN THE SERVICE INDUSTRY: A QUALITATIVE STUDY , Cheryl DePonte

EVALUATING HEALTHCARE STUDENT LEARNING PERFORMANCE DURING THE INITIAL YEAR OF THE COVID-19 PANDEMIC: A CASE STUDY , Maria D. Garcia-Villarreal

LEADERSHIP BEHAVIORS, PRACTICES, AND SYTLES IN MERGERS AND ACQUISITIONS IN THE U.S. TECHNOLOGY-BASED ORGANIZATIONS: A QUALITATIVE STUDY , SUSAN E. GLOVER

THE IMPACT OF THE COVID-19 PANDEMIC ON EMPLOYEE ENGAGEMENT AND PERFORMANCE IN THE TELEWORKING CONTEXT IN THE U.S. PUBLIC SECTOR: A PHENOMENOLOGICAL CASE STUDY , Elizabeth Nesuda

Theses/Dissertations from 2022 2022

Exploring the Roles of the Craft Trainer in the Construction Industry , Mary M. Chatham

PREPARE FOR THE WORST, HOPE FOR THE BEST: A QUALITATIVE STUDY ON WORKPLACE VIOLENCE IN THE HEALTH CARE INDUSTRY , John Haymore

WORKPLACE FUN FOR EMPLOYEE ENGAGEMENT: A FUNCTION OF ORGANIZATIONAL CULTURE? , Lacey Logan

TESTING THE PREDICTIVE VALIDITY OF A MANAGERIAL COACHING SCALE USING A CROSS-LAGGED PANEL DESIGN , Katherine Stone

Theses/Dissertations from 2021 2021

EFFECT OF TRAINING OPPORTUNITY AND JOB SATISFACTION ON TURNOVER INTENTIONS AMONG GEN X AND GEN Y , Regin Justin

The Effects of Perceived Organizational Justice of Inclusive Talent Management Practices on Employee Work Effort , Thomas Kramer

MENTORING EARLY CAREER TEACHERS UNDER COVID-19 PANDEMIC IN THE STATE OF TEXAS: A PHENOMENOLOGICAL CASE STUDY , Sonya H. Niazy

Theses/Dissertations from 2020 2020

EXAMINING MANAGERIAL COACHING DYADS AND THE DEVELOPMENTAL LEARNING OUTCOMES FOR MANAGERS SERVING AS COACHES AND THE REVERSE COACHING BEHAVIORS OF THEIR SUBORDINATE COACHEES , Beth Adele

Team-Based Effects on Individual Human Capital: A Proxy for Organizational Performance , Rob Carpenter

Testing the Modality Effect in an Online Training of Virtual Workers: An Experiment Inspired by Social Distancing , Janice Lambert Chretien

Examining the Mediating Effect of Job Crafting on the Relationship Between Managerial Coaching and Job Engagement in the Skilled Trades , Jennifer H. DuPlessis

PSYCHOLOGICAL WELL-BEING DURING RETIREMENT TRANSITION AND ADJUSTMENT FOR SOUTHERN BAPTIST PASTORS: A PHENOMENOLOGICAL MULTI-CASE STUDY , Tresa Gamblin

The Impact of Work Alienation on the Relationship Between Person-Organization Fit and Organizational Citizenship Behavior in Higher Education , Andrew R. Krouse

Antecedents to Strategic Project Success: A Qualitative Phenomenological Analysis of Project Leaders' Perceptions , Dave Silberman

Theses/Dissertations from 2019 2019

EXAMINING THE UNITED KINGDOM’S SOFT LAW APPROACH FOR WOMEN ON BOARDS WITH REGARD TO GENDER DIVERSITY AND THE GENDER PAY GAP: A REGRESSION DISCONTINUITY DESIGN , Silvana Chambers

ORGANIZATIONAL COGNITION AS INTERVENED BY ORGANIZATIONAL SUPPORT AND ENGAGEMENT ON MEDICAL CODERS’ EXHIBITION OF ORGANIZATIONAL CITIZENSHIP BEHAVIORS , David W. Conley

EXPLORING GRIEF AND MOURNING IN WORK TEAMS: A PHENOMENOLOGICAL MULTI-CASE STUDY , Ashley L. Kutach

EFFECTS OF THE DIMENSIONS OF QUALITY OF WORK LIFE ON TURNOVER INTENTION OF MILLENNIAL EMPLOYEES IN THE U.S. , Julie Lewis

EXAMINING THE DIRECT EFFECT OF CEO PERCEPTIONS OF COLLECTIVE ORGANIZATIONAL ENGAGEMENT ON PATIENT EXPERIENCE IN ACUTE-CARE HOSPITALS , Mary Lynn Lunn

SUCCESS AND FAILURE RATES, FACTORS, AND ALIGNMENT WITH CHANGE MODELS: A META-ETHNOGRAPHIC ANALYSIS OF PLANNED ORGANIZATIONAL CHANGE QUALITATIVE CASE STUDY LITERATURE , Diana McBurnett

- Collections

- Disciplines

Advanced Search

- Notify me via email or RSS

Author Corner

- Submit Research

- UT Tyler Human Resource Development PhD Degree

Home | About | FAQ | My Account | Accessibility Statement

Privacy Copyright

You're reading a free article with opinions that may differ from The Motley Fool's Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Cathie Wood Thinks This Artificial Intelligence (AI) Stock Can Soar by 1,082%. Here's Why I Think It Could Run Even Higher Than That.

- Cathie Wood sees Tesla's planned robotaxi fleet as its next major catalyst.

- Beyond self-driving car technology, Tesla is investing heavily in other areas of artificial intelligence (AI) such as humanoid robotics.

- The energy storage business is the fastest growing part of the company, yet it feels as if it's being ignored by the prognosticators.

- Motley Fool Issues Rare “All In” Buy Alert

NASDAQ: TSLA

Ark Invest's iconic boss just raised her five-year price target on Tesla stock to $2,600 per share.

2024 has been a tumultuous year for Tesla ( TSLA -6.55% ) investors.

For the first six months of the year, its shares drastically underperformed the S&P 500 and Nasdaq Composite as the stock cratered by roughly 20%. Nevertheless, longtime Tesla bull Cathie Wood of Ark Invest recently revised her price target for the EV stock. Wood is calling for Tesla shares to reach $2,600 by 2029 -- 1,082% higher than its recent level.

While some investors may argue such a forecast is outlandish, I personally think Wood may be underestimating Tesla's prospects.

Wood's thesis hinges on robotaxis, but...

Tesla is a pioneer among electric vehicle (EV) manufacturers. After making considerable headway over the last several years, the company is now laser-focused on what it expects will be its next chapter -- autonomous driving technology.

CEO Elon Musk is so compelled by the potential of autonomous driving that during the company's latest earnings call, he said: "I recommend anyone who doesn't believe that Tesla will solve vehicle autonomy should not hold Tesla stock. They should sell their Tesla stock. If you believe Tesla will solve autonomy, you should buy Tesla stock."

That's a polarizing statement, but those are pretty much par for the course with Musk. However, he isn't the only one with a strong conviction that autonomous driving is an enormous opportunity.

In Wood's latest model, she is projecting that subscriptions to Tesla's autonomous driving software -- dubbed full-self driving (FSD) -- will be the major catalyst for the company's future growth. In essence, FSD represents a source of high-margin recurring revenue for its EV operation.

Moreover, if the company ends up as the superior developer of self-driving technology , Tesla will have an enormous opportunity to disrupt areas such as rental car businesses, delivery services, and ride-hailing applications.

But while I understand the opportunities FSD presents, I think Wood is underestimating Tesla's long-run potential.

Image Source: Getty Images

...what about robotics and energy storage?

Autonomous driving is merely an extension of the EV business. But on a deeper level, FSD is an advanced application of artificial intelligence (AI). While Musk and his team remain steadfast in its FSD pursuits, Tesla has far more ambitions in the broader AI realm. In particular, it is developing a line of humanoid robots called Optimus. The idea is that it could enhance its efficiency and productivity by augmenting its human workforce with Optimus robots.

Should this effort prove successful, Tesla would have an incredibly lucrative opportunity to commercialize Optimus and sell robots to other companies. This could revolutionize the labor market -- and Wood does not seem to be accounting for that potential in her model.

The main reason why Wood isn't banking much on Optimus at the moment is that she believes commercialization of the robots is more than five years away. However, at the risk of being overly Pollyanna-ish, I think Wood may want to rethink that position. On Tesla's second-quarter earnings call , Musk said "we expect to have several thousand Optimus robots produced and doing useful things by the end of next year in the Tesla factories." He further predicted that in 2026 the company would be "ramping up production quite a bit" and selling them to external customers.

Beyond its AI initiatives, Tesla has already built a thriving energy storage business that I think is criminally underappreciated.

The table below breaks down the financial results for Tesla's energy generation and storage segment over the last several quarters.

| Category | Q2 2023 | Q3 2023 | Q4 2023 | Q1 2024 | Q2 2024 |

|---|---|---|---|---|---|

| Energy generation and storage revenue | $1.5 billion | $1.6 billion | $1.4 billion | $1.6 billion | $3.0 billion |

| Energy generation and storage gross margin | 18% | 24% | 22% | 25% | 25% |

Data source: Tesla.

Tesla has doubled its revenues from the energy storage business over the last year. But even more impressive, it has achieved strong unit economics, underpinned by a consistently expanding gross margin profile.

These dynamics are important because the growth in the energy storage segment is helping offset the stagnation and decline of its core EV business. Moreover, because it's generating strong and growing profits from its energy generation unit, Tesla is still able to invest in important growth initiatives -- particularly in AI.

Looking at Tesla's valuation

One thing that Wall Street analysts can't seem to agree on is Tesla's valuation. And on the surface, I totally get it. Its market capitalization is currently around $700 billion -- nearly 16 times that of Ford and 14 times the size of General Motors . Fundamentally, that doesn't really check out.

However, like Wood and Musk, I see Tesla as much more than a car company. Investors need to look at the different components of its overall operation and analyze their valuations individually. This is commonly referred to as a sum-of-the-parts valuation.

Beyond its EV segment, the company is making inroads in two areas with strong secular tailwinds : AI and sustainable energy. Admittedly, it has yet to really monetize its AI products at scale. For that reason, I understand if bearish investors remain skeptical. But as a Tesla shareholder for many years, I have a strong belief that the company will continue making progress toward FSD. Moreover, I think success in FSD will lead to a surge of demand as the company attempts to differentiate its fleet from the competition.

In addition, I'm compelled by the case around Optimus and am aligned with Musk on the premise that these robots will be commercialized sooner rather than later. Lastly, the energy storage business is growing faster than any other part of the company, and I don't see demand in that area slowing down anytime soon.

Whether or not the stock reaches Wood's price target on her forecast schedule is moot. In the long run, Tesla has a lot of opportunities to disrupt several more markets other than EVs, and I am bullish about its prospects for executing on its vision. For these reasons, I think Tesla is a strong buy for investors with a long-term time horizon.

Adam Spatacco has positions in Tesla. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends General Motors and recommends the following options: long January 2025 $25 calls on General Motors. The Motley Fool has a disclosure policy .

Related Articles

Premium Investing Services

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Human Subjects Office

July 2024 irb connection newsletter, irb efficiency initiatives and results to date, irb efficiency initiative: current and upcoming, herky hint: help messages, aahrpp accreditation: preparing for site visit interviews, course-related student projects: is irb approval required, learning opportunity: irb overview lecture in icon, in the news, upcoming educational events, irb efficiency initiative s and results to date, by kelly o’berry and michele countryman.

Beginning in January 2024, the Human Subjects Office (HSO) rolled out six major initiatives to improve Institutional Review Board (IRB) and Human Research Protection Program (HRPP) review processes. This article provides an evaluation of previous programming changes that were presented at the May IRB Efficiency Initiative Information Session .

Here’s a brief overview of the initiatives and results to date:

60-Day Withdrawal Due to PI Inactivity (effective 1/29/24): 1,059 New Project and Modification Forms submitted since implementation. Of these, 106 forms were withdrawn (10%), 17 were recreated, and 9 were resubmitted.

DSP Approval Timing (effective mid-February 2024): The new process for faster signoffs from the Division of Sponsored Programs allowed the release of HRPP approvals an average of 48 days earlier ( 36 days median).

Required Actions After the IRB Meeting (effective 4/1/24): the average time to provide the PI with required actions from IRB meeting minutes has gone from 9 days to less than 24 hours since April 1.

Assign a Meeting Date Goal (effective 4/1/24): Limited data is available, but 71% of studies met the date goal. More in-depth information will be available after the June rollout that separated IRB review from HRPP Committee Approvals.

60-Day Withdrawal Due to PI Inactivity (effective 1/29/24)

HawkIRB forms are automatically withdrawn if there is no response to workflow in 60 days . This change will allow for more accurate metrics for IRB review time.

In addition to the two-week reminders, a new 55-day HawkIRB email notice states that the form will be withdrawn in five days. The form in the PI’s inbox shows the number of days in Workflow over the total days since submission. At 55 days , the form is highlighted in red in the PIs inbox.

Evaluation data for New Project forms and Modification forms:

The 106 withdrawn forms represent a considerable timesaving for HSO staff reviewers. Most withdrawn forms have not been recreated and very few recreated forms have been submitted to the IRB.

NOTE: For a withdrawn form, the PI can only use the “recreate” link once. It is best to hold off on recreating the form until all issues that were holding up the response to the workflow questions in the original form have been resolved.

DSP Approval Timing (effective mid-February 2024)

Division of Sponsored Programs (DSP) approval is required in HawkIRB for industry-initiated, industry-funded clinical trials where a research contract is required to document institution and sponsor expectations. The research application can be approved by the IRB, but not released to the study team until DSP approval is documented. In February, DSP updated their “contract approval” process for these industry-sponsored clinical trials. DSP approval used to be documented when the contract was fully executed; contract negotiations were complete, all signatures in place (institution, PI, and sponsor), and budget approved. Now DSP issues approval in HawkIRB when contract negotiations are complete, even if signatures and/or budget remain pending. This removed a significant delay in the HRPP approval process. Note: The PI must continue to work with the sponsor to obtain signatures and finalize the budget prior to initiating the research.

This change affected 38 studies from mid-February to early June. Faster DSP sign off allowed the release of HRPP approvals 48 days earlier than the previous average. For these studies, the median turnaround for IRB approval was 36 days , which is considerably below the goal of a 45-day median from submission to approval for full board review.

Assign a Meeting Date Goal (effective 4/1/24)

Application Analysts can now set an IRB meeting date goal, and a due date for meeting this goal, at the beginning of the IRB review process.

NOTE: There were several limiting factors for evaluation of this change. IRB meeting agendas were full through April 22 when this change took effect on April 1. The first New Project form included in this evaluation was submitted on April 2 and scheduled to a meeting on May 9. This evaluation is based on data from early May through mid-June.

Also, when this change took effect the hold for three Human Research Protection Program (HRPP) committees prevented scheduling forms to an IRB meeting. The IRB Efficiency Initiative rollout on June 14, 2024, lifted this hold by separating the IRB and HRPP Committee approvals. Future data will provide a more in-depth evaluation.

Required Actions After the IRB Meeting (effective 4/1/24)

HSO staff can now provide required actions to the PI shortly after the IRB meeting, which gives the PI/research team a head start to address required actions before receiving the full set of IRB meeting minutes.

Before April 1, 2024, the average time to provide required actions to the PI in the full meeting minutes was 9 days. The goal is to provide required actions within 24 hours and the full set of meeting minutes within four business days.

Of 167 sets of meeting minutes completed between April 1 and mid-June, HSO staff effectively decreased the average time to provide required actions to the PI to less than 24 hours. The research community has provided positive feedback about this change.

Seventeen sets of minutes (10%) did not meet the goal due to the complexity of the issues the board discussed. Approximately half of these minutes were from a monthly IRB-01 Executive Committee meeting. The Executive Committee reviews more complex study design and compliance-related issues.

IRB Efficiency Initiative Announcements and Updates

See IRB Efficiency Initiative Announcements and Updates for information about o ther initiatives that are in progress or have been implemented since June 2024, including: launching the new HSO website , adding a chair designee to assist with IRB-02 post-approval forms, onboarding a new IRB-02 chair, Primary Reviewer process enhancements and more.

By Kelly O’Berry and Michele Countryman

The IRB Efficiency Initiative rollout in June 2024 separated IRB review and approval from the other Human Research Protection Program (HRPP) committee approvals. This article provides an overview of that change and a summary of other initiatives in progress, updated documents, policies and procedures and information session/demonstration recordings.

Separate IRB and HRPP Committee Approvals - June 2024 Rollout

HawkIRB programming changes rolled out June 14, 2024, separated IRB review and approval from other HRPP Committee approvals. Prior to this change, the IRB could not begin the convened board review process until the issuance of approval from three committees/entities: Conflict of Interest in Research (CIRC) , Protocol Review and Monitoring Committee (PRMC, in Holden Comprehensive Cancer Center) , and Research Billing Compliance (RBC) . The HSO can now schedule a New Project or Modification form to a convened IRB meeting before the completion of these HRPP committee reviews/approvals.

The second programming change allows the IRB to grant full IRB approval before the issuance of all HRPP approvals. Prior to this efficiency initiative, the IRB would hold approval pending approval from these additional HRPP committees: Pharmacy & Therapeutics (P&T) , Medical Radiation and Protection Committee (MRPC) , Institutional Biosafety Committee and Nursing Research Committee (NRC) . Additionally, the IRB can now grant approval before the Division of Sponsored Programs (DSP) signs off on the grant or contract.

The Principal Investigator (PI) can now submit a Modification form in HawkIRB to address requests from HRPP Committees that complete their review after the IRB approves the New Project form. The New Project form is released when the Modification form is approved and released in HawkIRB.

Several documents, policies and procedures were updated or added in June. See a detailed list at the end of this article .

What’s Next for the IRB Efficiency Initiative?

The following initiatives are in progress or have already been implemented since the June IRB Efficiency Initiative Information Session:

New IRB review and approval structure for IRB-02 (social/behavioral research) – Effective at the start of Fiscal Year 2025, we added an IRB Chair Designee to assist with approval of post approval forms (e.g., Modification, Continuing Review, or Modification/Continuing Review) meeting an expedited or exempt criteria for approval. This enhancement is consistent with a long-standing IRB-01 review structure and is consistent with IRB practices across the nation. The new IRB-02 Chair Designee is an experienced IRB member who is already serving as an IRB-01 Chair Designee.

New IRB-02 Chair – The new IRB-02 Chair, an experienced IRB member, will begin onboarding and training in August as part of succession planning for IRB-02 Chairs.

Primary Reviewer process enhancements for full board review – HawkIRB programming is underway to update the Primary Reviewer Checklist used at convened board meetings and enhance the training process for Primary Reviewers.

HawkIRB Application Redesign – This initiative to streamline the HawkIRB application began with the rollout of Section III updates on January 29, 2024. The goal is to make forms easier for researchers to complete and more efficient for the IRB review. This is a continuation of the 2022-2023 initiative to update the HawkIRB form for projects that qualify for Exempt Status. The next HawkIRB application redesign rollout will focus on updates to the single IRB review process. This is in preparation for the anticipated FDA adoption of the revised Common Rule regulations regarding the use of a single IRB for multi-site projects.

New HSO website – The new HSO website is now live! HSO staff are still making final tweaks and corrections to URLs. It will take time for search engines to only identify pages of the new website. Use the gold buttons on the home page and the menu options to find what you need. We welcome your feedback. For assistance with finding anything on the new website or to provide feedback, please contact us at [email protected].

AAHRPP Accreditation Site Visit – 2024-2025 is our HRPP reaccreditation period and will involve a significant amount of HSO time and resources. There are two steps in the reaccreditation process. The UI is currently at Step I; the initial application was submitted in March, and we are currently responding to AAHRPP review of submission materials. Step II is the site visit which will occur this fall. The site visit includes interviews with select PIs and research staff. See February through July IRB Connection Newsletter articles for additional information about accreditation and preparing for the site visit.

Announcements and Updated Resources

The following documents were updated or added during the June IRB Efficiency Initiative rollout:

New Resources:

Other HRPP Committee Tool – Includes an organizational chart, information about each committee and when their review is required, and regulatory references for these reviews. [Link at end of first paragraph]

HRPP Committee Review Process Flow Chart – Illustrates the timing of steps in the IRB review process and HRPP committee approvals. [Link in first sentence of the second full paragraph]

UI IRB Standard Operating Procedures and Researcher Guide

Updated Policies and Procedures:

External IRB Standard Operating Procedures

VA Researcher Guide

May 2024 IRB Efficiency Initiative Information Session (recording)

Trainings and Demos:

HawkIRB demo: Separating IRB and HRPP Committee Approvals (recording)

WCG Training (recording, June 19, 2024)

IRB ICON Course for Researchers – Slides, recordings, demo recordings and instruction documents

Herky Hint: Help Messages

By rachel kinker, mpa.